𝗛𝗼𝘄 𝗔𝘀𝘀𝗲𝘁 𝗠𝗮𝗻𝗮𝗴𝗲𝗿𝘀 𝗨𝘀𝗲 𝘁𝗵𝗲 𝗔𝗹𝘁𝗺𝗮𝗻 𝗭-𝗦𝗰𝗼𝗿𝗲 𝗽𝗹𝘂𝘀 𝘁𝗼 𝗣𝗿𝗲𝗱𝗶𝗰𝘁 𝗖𝗼𝗿𝗽𝗼𝗿𝗮𝘁𝗲 𝗗𝗶𝘀𝘁𝗿𝗲𝘀𝘀?

One of the most effective tools for assessing corporate bankruptcy risk is the Altman Z-Score. Developed by Edward Altman in 1968, this financial metric helps investors and lenders gauge a company’s financial health by analyzing liquidity, profitability, leverage, and efficiency.

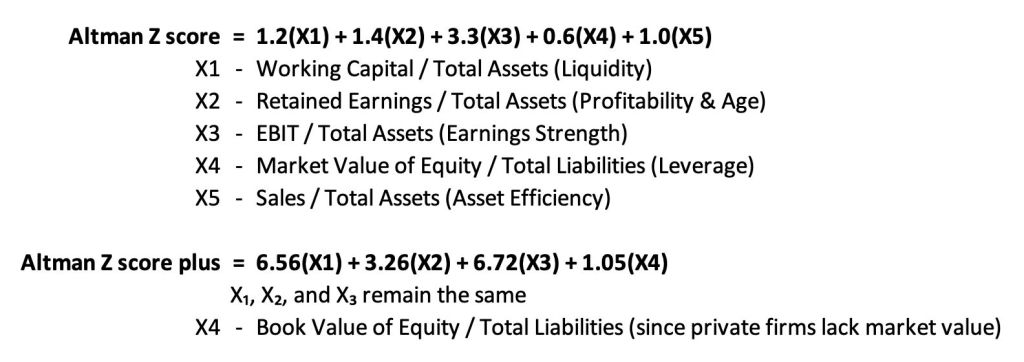

Z-Score for Public Manufacturing Firms (Original Model)

Z = 1.2(X1) + 1.4(X2) + 3.3(X3) + 0.6(X4) + 1.0(X5)

Z-Score Plus for Non-Manufacturing & Private Firms

To improve applicability to non-manufacturers and private firms, the model modifies the equation:

Z’ = 6.56(X1) + 3.26(X2) + 6.72(X3) + 1.05(X4)

𝗛𝗼𝘄 𝗜𝘁 𝗪𝗼𝗿𝗸𝘀

The Z-Score combines five financial ratios to classify firms into three zones:

✔ Safe Zone (Z > 2.99) – Low risk of financial distress

⚠ Gray Zone (1.81 < Z < 2.99) – Moderate risk

❌ Distress Zone (Z < 1.81) – High risk of bankruptcy

𝗛𝗼𝘄 𝗔𝘀𝘀𝗲𝘁 𝗠𝗮𝗻𝗮𝗴𝗲𝗿𝘀 & 𝗛𝗲𝗱𝗴𝗲 𝗙𝘂𝗻𝗱𝘀 𝗨𝘀𝗲 𝗜𝘁

1. Distressed Debt Investing – Hedge funds identify companies with low Z-Scores, buy their debt at a discount, and profit from restructurings or recoveries.

2. Long-Short Equity Strategies – Investors short stocks of firms with weak Z-Scores (financially unstable) and go long on companies with strong Z-Scores.

3. Credit Risk Assessment – Asset managers use Z-Scores to assess bond risks and avoid issuers with high default probability.

𝗥𝗲𝗮𝗹-𝗪𝗼𝗿𝗹𝗱 𝗘𝘅𝗮𝗺𝗽𝗹𝗲𝘀

1. Lehman Brothers (2008) – Z-Score signalled financial distress before bankruptcy.

2. Tesla (2020-2023) – Initially had a weak Z-Score but improved as profitability surged.

3. Sovereign Debt Analysis – Some investors use country-level adaptations of the Z-Score to assess national credit risk.

𝗪𝗵𝘆 𝗜𝘁 𝗠𝗮𝘁𝘁𝗲𝗿𝘀

In a volatile market, risk management is critical. The Altman Z-Score remains a powerful, transparent, and reliable tool for making informed investment decisions.

𝗣𝗮𝗽𝗲𝗿 𝗿𝗲𝗳𝗲𝗿𝗿𝗲𝗱: “𝗘𝗱𝘄𝗮𝗿𝗱 𝗜. 𝗔𝗹𝘁𝗺𝗮𝗻, 𝗣𝗵𝗗: 𝗙𝗶𝗳𝘁𝘆 𝗬𝗲𝗮𝗿𝘀 𝗼𝗳 𝗭-𝗦𝗰𝗼𝗿𝗲𝘀 𝘁𝗼 𝗣𝗿𝗲𝗱𝗶𝗰𝘁 𝘁𝗵𝗲 𝗣𝗿𝗼𝗯𝗮𝗯𝗶𝗹𝗶𝘁𝘆 𝗼𝗳 𝗖𝗼𝗿𝗽𝗼𝗿𝗮𝘁𝗲 𝗕𝗮𝗻𝗸𝗿𝘂𝗽𝘁𝗰𝘆”